In Support of Pete Hegseth

— Organisation: The Claremont Institute —Secretary of War Pete Hegseth is under attack from practically all sides. The Left has been after him since before his confirmation hearing. Some on the Right have likewise been lukewarm since Trump picked him, with interventionists hoping for one of their own such as Senator Tom Cotton, and restrainers wanting a candidate who aligns with their views. Throughout his tenure, the press has placed Hegseth under a magnifying glass, reporting on a long list of supposed controversies, which now includes his daring to fire generals and his willingness to carry out President Donald Trump’s orders in Iran. As the pressure has built, leaks against Hegseth, and even some calls for his firing, have begun to seep into the press.

President Trump should resist these efforts. Not only would firing Secretary Hegseth be a mistake, but doing so would undercut, and potentially even put an end to, his revolution against the uniparty.

Try, Try Again

President Trump faces a still-powerful military-industrial complex, as well as a hardened political establishment that backs it. He should learn from Andrew Jackson, both a former president and a political revolutionary, who came to understand how important it was to have loyal people around him.

AnnouncementOnline Workshop: Money in the Digital Age with Prof. Benjamin Geva (Apr. 22)

— Organisation: Just Money — Evolution and Future of Money in Canada: Implications for the Digital Age, Legal and Regulatory Perspective

More “Announcement

Online Workshop: Money in the Digital Age with Prof. Benjamin Geva (Apr. 22)”

What’s On Apr 6-12 2026

— Organisation: Free Palestine Melbourne —04/07/2026 Market Update

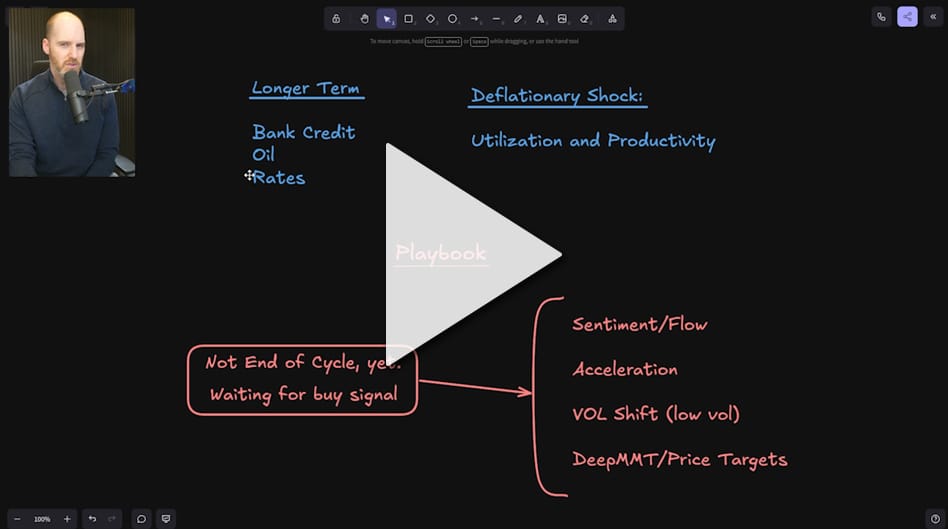

— Organisation: Applied MMT —Preview

Markets finally got the catalyst they needed.

Tonight’s ceasefire announcement between the Trump administration and Iran has sparked the sort of move that can change the short-term character of this market very quickly. Equities responded exactly how you would expect when a major pocket of uncertainty gets lifted: aggressively, and all at once.

The bigger point, though, is that this rally did not come out of nowhere. The data was already getting very close to a proper turn. Tonight’s news may have simply been the final push that kicked off the move we had been waiting for. In the full update below, I go through the playbook, where the buy signals stood before tonight, what this changes, what still needs to be watched, and why I think this likely marks the beginning of the next leg higher.

Yanis Varoufakis on misogyny, resistance and why everything could be different

— Organisation: The Australia Institute —On this episode of Follow the Money, we bring you highlights from the recent Australian tour of economist and author Yanis Varoufakis, with contributions from a cast of very special guests. Across live events in Adelaide, Sydney and Melbourne, they discuss misogyny, political power, the erosion of Palestinian rights, and Yanis’ latest book, Raise Your Soul: A Personal History of Resistance.

Become an Australia Institute supporter today.

Guest: Yanis Varoufakis, economist & author // @yanisvaroufakis

Guest: Clare Wright OAM, Professor of History and Professor of Public Engagement, La Trobe University // @clarewrighthistorian

Guest: Randa Abdel-Fattah, Future Fellow in Sociology, Macquarie University // @RandaAFattah

Guest: Richard Denniss, co-Chief Executive Officer, the Australia Institute // @richarddenniss

Social Democrats of the North: École Sociale Populaire

— Publication: Perspectives Journal —Listen to the full conversation on the Perspectives Journal podcast, available to subscribe on Spotify, Apple Podcasts, YouTube, Amazon Music, and all other major podcast platforms.

The War in Iran Is a Mistake

— Organisation: The Claremont Institute —No mere politician in modern history has had a wartime general’s capacity for decision-making amid chaos like President Trump. His force of character (“Fight! Fight! Fight!”) and his appeal to the everyman (with the boorishness thereof) reveal an instinctual giant who is at his best while disorder surrounds him.

However, one who thrives in chaos often rejects the peace and order of civilization and tends to gravitate to the home turf of mayhem. Consequently, Trump may still pull a rabbit out of the hat in Iran. But the odds continue to stack against him.

The American people voted for him multiple times on his assurance of peace and promises of foreign adventurism to be a thing of the past. As Trump repeatedly noted on the campaign trail, American blood and treasure had been treated far too cheaply by both Presidents Bush and Obama. He vowed to stop that bipartisan trend.

Is the War In Iran About to Become Apocalyptic? (w/ Trita Parsi) | The Chris Hedges Report

— —This interview is also available on podcast platforms and Rumble.

Recently, United States President Donald Trump has been issuing a series of soft deadlines to pressure Iran to fully open the Strait of Hormuz. On Easter Sunday, in what would be a serious escalation of the conflict, President Trump threatened to target “bridges and power plants” and to “bomb Iran back to the Stone Age” beginning on Tuesday if Iran refuses his demands. To better understand what the ramifications would be if President Trump follows through on his threats, Chris Hedges sits down with Trita Parsi, an expert on US-Iranian relations and the geopolitics of the Middle East.

Invernadero para el Desarrollo: Reordenando la Economía Mixta y el Capitalismo de Estado

— Publication: Progress in Political Economy — En 1999, el Servicio Postal Mexicano, que por entonces era de propiedad estatal, emitió un sello conmemorativo para celebrar los sesenta y cinco años del banco de desarrollo ‘Nacional Financiera’ (Nafin) de México.

En 1999, el Servicio Postal Mexicano, que por entonces era de propiedad estatal, emitió un sello conmemorativo para celebrar los sesenta y cinco años del banco de desarrollo ‘Nacional Financiera’ (Nafin) de México.

The Fed Has Two Tools to Influence Money Market Conditions

— Organisation: Federal Reserve Bank of New York — Publication: Liberty Street Economics —“Values” Are Not the Answer

— Organisation: The Claremont Institute —What is it, according to Francis Fukuyama, “for which we should be willing to struggle and die today,” and how does history—Western civilization—inform our answer to this permanent question?

Fukuyama thinks history has bequeathed us liberal “values” sufficient for the purpose. Spencer Klavan thinks history has quite a bit more to offer. Fukuyama has made a career out of the “end of history.” Klavan points the way to careers for young Americans in the continuation and making of history. He thinks the 250th anniversary of American independence is a good time for Americans to reflect on how Western civilization has always informed our answer to this question and continues to do so.

Nothing could be more edifying for Americans than a true and sufficient answer to the unsettling question of what they should be willing to fight and die for. Klavan thinks that if Americans are to be properly edified, they will “need to recover a sense of their country as an era-defining project, forward-looking but steeped in ancient traditions of faith and law—not just a Western nation, but the Western nation par excellence.” Here, to quote Walter Berns, I will hope to do “nothing but edify.” Berns gave that phrase currency among small circles back in the early 1980s, accusing Harry Jaffa of misunderstanding Leo Strauss when Jaffa claimed Strauss thought philosophy, or even political philosophy, might have some place in saving Western civilization—and America.

The Renegade Academy

— Organisation: The Claremont Institute —When Allen C. Guelzo and James Hankins began writing The Golden Thread, their two-volume History of the Western Tradition, they were both Ivy League professors. By the time it was published, neither of them was. Hankins, whose first volume on The Ancient World and Christendom sweeps from Greco-Roman and Jewish antiquity to the European Renaissance, gave his last lecture as a history professor at Harvard late last year. Guelzo, whose second volume on The Modern and Contemporary West begins with the Protestant Reformation and ends hauntingly with images of the World Trade Center shortly before its destruction, left Princeton last fall. Both authors are now faculty members at the University of Florida’s Hamilton School for Classical and Civic Education, established in 2022. The Golden Thread is a momentous achievement. It’s also a landmark event in the history of American letters. Its appearance signals that the country’s most prestigious universities have all but given up on maintaining the intellectual foundations of the West. For the time being, perhaps, the stewards of civilization will have to do their work outside the gates of the old academy. They will have to build something new.

***

No Right Is Ever Safe – but Progress Is Possible

— —

Will There be a Ground Invasion of Iran? (w/ Col. Larry Wilkerson) | The Chris Hedges Report

— —This interview is also available on podcast platforms and Rumble.

More than one month into the American-Israeli war on Iran, the US military has expended a significant amount of its arsenal and many billions of dollars without making any progress in meeting its illusory and often-changing objectives. As the White House and Pentagon, and the markets, panic, the United States has begun deploying troops and resources to the region in preparation for a possible ground assault. This raises significant questions about what type of campaign the US is capable of waging and whether, as analysts are saying, fighting the Iranian military on its own terrain would be a bloodbath for US troops. Would putting boots on the ground embroil the US in another prolonged quagmire, similar to other recent US wars in the region, that would end in defeat?

How I ended up defining demagoguery as I do

— —

Why does demagoguery matter? And why does it matter how we define it?

What DeepMinsky Says About the Oil Shock: A Market Simulation

— Organisation: Applied MMT —Why Rising Oil Prices May Not Break This Market

Last night, Donald Trump delivered an address to the nation, offering an update on the ongoing conflict with Iran. The takeaway, at least from my perspective, was fairly clear: the message to the rest of the world was essentially, you deal with the Strait of Hormuz, while we may still have more to do with Iran. Markets initially did not like that framing at all.

Futures sold off heavily overnight. But interestingly, by the time the regular session unfolded, we saw a strong recovery. In fact, from the lows we saw on Friday to where things stand now, the S&P 500 has bounced roughly 4%. That raises an important question: are markets beginning to stabilize, even with oil continuing to surge?

Because while equities have started to recover, oil has been having another explosive move higher. As I’m writing this, WTI is sitting around $113 per barrel, and markets are clearly preparing for the possibility that prices could climb further. The issue now is no longer just whether oil is rising, but what that rise actually means for growth, inflation, and the broader market outlook.

Is Iran the 'Leading State Sponsor of Terrorism?' (w/ John Kiriakou) | The Chris Hedges Report

— —This interview is also available on podcast platforms and Rumble.

In an attempt to justify and garner popular support for the American-Israeli war on Iran, the Trump administration is pressuring its allied nations to join the US in designating Iran’s Revolutionary Guard Corps as the world’s greatest sponsor of state terrorism. The administration points to Iran’s participation in the Axis of Resistance, which includes Hezbollah in Lebanon, Hamas in Palestine and Ansar Allah in Yemen, as evidence for its position. This raises the question of whether Iran, by supporting proxy organizations, is doing anything differently from what US intelligence agencies have done for many decades.

How the Beltway Media Machine Works

— Organisation: The Claremont Institute —It’s a running joke in the Beltway that defense contractors put up billboards advertising, say F-35s, at the Pentagon City metro station. Your everyday commuter, even in Washington, isn’t picking up fighter jets off the shelf at Costco on Sundays. But a chunk of the people who work on defense contracts will pass through the Pentagon’s metro stop, and Lockheed Martin knows this.

In theory, the same logic fuels D.C.’s media business. In the last two decades, the capital city has become dominated by a constellation of powerful media outlets that deliver niche, social-media-based coverage of the federal government. Think Politico, Semafor, Punchbowl News, and Axios (the latter two evolved directly from the Politico model).

These publications produce insider email newsletters that cover the daily pulse of Capitol Hill, energy policy, foreign affairs, and the White House, and are written specifically for staffers, journalists, and lobbyists. Playbook famously includes a birthday list every morning; that’s how small the audience is relative to other national publications. Web 2.0 made this business model possible, and it’s only grown as mass media flails.

Talent We Already Have: Unlocking Productivity Through Migration

— Organisation: Per Capita —By Dr Wesa Chau, Executive Director

Yesterday I listened to Violet Roumeliotis AM and Dr Martin Parkinson speak at the National Press Club about skills shortages, productivity, and the persistent underutilisation of migrant skills in Australia. Their discussion highlights a fundamental contradiction in Australia’s labour market: at a time of acute workforce shortages and slowing productivity growth, we are failing to make effective use of the skills already within our borders. This is not simply an issue of fairness or social inclusion—it is a structural economic failure.

This reality is not surprising to me. Having worked with migrants, refugees, and international students for over 25 years, I have seen countless examples of people who are highly capable, qualified, and motivated, yet unable to secure employment commensurate with their skills. Too often, opportunities are denied because of an accent, a lack of so‑called “Australian experience”, or unfamiliar qualifications—barriers that are cultural and systemic rather than reflective of actual competence.

A missed opportunity | Between the Lines

— Organisation: The Australia Institute —The Wrap with Dr Emma Shortis

What a missed opportunity.

Last night, the Australian Prime Minister had the chance to face reality. His address to the nation was a recognition that Australians are deeply worried about the state of the world – as they should be. Our world is in real trouble, and there is every indication that the trouble is going to get worse.

What the prime minister did not say is that this trouble lies at the feet of the President of the United States.

Photo: AAP Image/Lukas Coch

— Dr Emma Shortis is Director of The Australia Institute’s International & Security Affairs Program.

It’s time to tax gas properly

— Organisation: The Australia Institute —On this episode of Dollars & Sense, Greg and Elinor discuss the prime minister’s national address on the impacts of the US-Israel war on Iran, policy responses to fuel price hikes, Australia’s gas giveaway and Greg’s visit to a gas conference.

This discussion was recorded on Thursday 2 April 2026.

Check out our Australia’s Gas Giveaway live tracker.

Host: Greg Jericho, Chief Economist, the Australia Institute // @grogsgamut

Host: Elinor Johnston-Leek, Senior Content Producer, the Australia Institute // @elinorjohnstonleek

Show notes:

Prices skyrocket but major fuel shortages “very unlikely”, Follow the Money (April 2026)

Australia’s land value has gone through the roof. Where does that leave young people who want to buy a home? by Greg Jericho, Guardian Australia (April 2026)

Treasury Market Liquidity Since April 2025

— Organisation: Federal Reserve Bank of New York — Publication: Liberty Street Economics —

In this post, we examine the evolution of U.S. Treasury market liquidity over the past year, which has witnessed myriad economic and political developments. Liquidity worsened markedly one year ago as volatility increased following the announcement of higher-than-expected tariffs. Liquidity quickly improved when the tariff increases were partially rolled back and then remained fairly stable thereafter (through the end of our sample in February 2026), including after the recent Supreme Court decision striking down the emergency tariffs and the subsequent announcement of new tariffs.

The American Mind Podcast: The Roundtable Episode 311

— Organisation: The Claremont Institute —The American Mind’s ‘Editorial Roundtable’ podcast is a weekly conversation with Ryan Williams, Spencer Klavan, and Mike Sabo devoted to uncovering the ideas and principles that drive American political life. Stream here or download from your favorite podcast host.

Congress Take the Wheel | The Roundtable Ep. 311

Deserving Success: America at 250

— Organisation: The Claremont Institute —Spencer Klavan’s thoughtful reflections on America and its future are measured and understated, reflecting the general mood of ambivalence and uncertainty surrounding the nation’s 250th birthday. Those of us old enough to remember the 1976 Bicentennial have been struck by the dissimilarity in the public mood. Julie Ponzi, writing for Chronicles, noticed this back in 2024: “The hype surrounding both the 1976 Bicentennial and the 1987 Bicentennial of the U.S. Constitution was so intense that both events inspired in me an intense interest and curiosity about American history.” Now that the semiquincentennial year is officially upon us, the lack of enthusiasm is even more evident. We don’t seem to know what we should be celebrating, or even whether we should.

What the Story of Salem Mason Tells Us About Nashville

— —Prices skyrocket but major fuel shortages “very unlikely”

— Organisation: The Australia Institute —Matt Grudnoff and Ebony Bennett discuss Australia’s relatively strong position in global energy supply chains. Matt explains why some petrol stations have run low despite overall fuel supplies remaining steady, how the price hikes are fuelling inequality, and why Scott Morrison’s 2021 claim about an electric vehicle policy putting an “end to the weekend” now looks even more absurd than it did at the time.

This episode was recorded on Tuesday 31 March.

You can sign the Australia Institute’s petition calling on the federal government to make gas exporters pay their fair share.

Guest: Matt Grudnoff, Senior Economist, the Australia Institute // @mattgrudnoff

Host: Ebony Bennett, Deputy Director, the Australia Institute // @ebonybennett

Show notes:

Fuel costs and RBA hikes equal to a 90 basis point rate rise: ‘this is brutal’ by Greg Jericho, The Point (March 2026)

Webinar: ‘Breaking the Chain: Freedom for Palestinian Political Prisoners’ (15 April)

— Organisation: Free Palestine Melbourne —Albanese Government introduces Unfair Trading Prohibition

— Organisation: Consumer Policy Research Centre —The post Albanese Government introduces Unfair Trading Prohibition appeared first on CPRC.

American Renewal and the Continuity of the West

— Organisation: The Claremont Institute —It is a pleasure to respond to Spencer Klavan’s graceful and inspired reflections on the prospects for America as we move closer to the 250th anniversary of the founding. He admirably eschews polemics and avoids an excessively narrow preoccupation with the most heated issues of the day, concerning himself with broader and deeper matters. At the same time, he writes as a partisan of the American project and the broader civilization—Western civilization—of which it has been a particularly vital and noble expression. Klavan raises big questions without succumbing to fashionable, or once-fashionable, theses such as “The End of History” or the ideological temptation of Year Zero-ism, which distort the past and present, as well as the prospects for the future.

Seizing the Working Class Opportunity in AI Data Centers

— Organisation: The Claremont Institute —As AI continues its explosive growth, data centers are becoming the primary target of backlash. From rural Louisiana to the suburbs of Arlington, Virginia, Americans are showing up at zoning and permitting boards to challenge their construction. Bernie Sanders has called for a nationwide data center moratorium, while Republicans in Florida propose regulating their energy and natural resource use.

The criticisms so far have centered on claims about the data centers’ water consumption, electricity demand, noise pollution, land use, and overall disruption—issues that tech companies like Meta are working to address with new practices and community investments. Yet something more needs to be done on the political front to ameliorate Americans’ growing concerns about data centers.

Aussies want investor tax breaks cut and more social housing built, polling reveals

— Organisation: Everybody's Home —Most Australian voters want the government to reduce tax breaks for property investors and put more money into social housing, according to new polling.

It comes as new analysis from Everybody’s Home also found that these tax breaks have fuelled a landlord boom with more than one million now reaping the benefits, yet housing affordability has never been worse.

The polling conducted for The Australia Institute in March found of the 1,502 Australians surveyed:

Behind the ATM: Exploring the Structure of Bank Holding Companies

— Organisation: Federal Reserve Bank of New York — Publication: Liberty Street Economics —Editor’s note: The fifth and sixteenth paragraphs have been revised for technical accuracy. April 8, 2026, 5:00 p.m.

Chris Hedges Q&A at Princeton University: Iran, Gaza and the Future of American Foreign Policy

— —The US has left itself with no good options in Iran

— Organisation: The Australia Institute —On this episode of After America, Dr Emma Shortis and Angus Blackman discuss the situation with the Strait of Hormuz, Israel’s invasion of Lebanon, why airport security workers in the US aren’t getting paid, and why, despite plenty of evidence suggesting it’s a terrible deal, some Australian policymakers remain committed to the bit with AUKUS.

This episode was recorded on Monday 30 March.

Host: Emma Shortis, Director, International & Security Affairs, the Australia Institute // @emmashortis

Host: Angus Blackman, Executive Producer, Podcasts, the Australia Institute // @angusrb

Show notes:

Shorter America This Week: Maximum Lethality; Everything has a history; Don’t fly with me by Emma Shortis, The Point (March 2026)

Trump is impotently railing against the US’s allies. Albanese is right to avoid the president’s global catastrophe by Allan Behm, The Point (March 2026)

Living Under the Feminist Gaze

— Organisation: The Claremont Institute —Every couple of years, another hit piece surfaces to explain why the Right supposedly hates women and why women on the Right hate themselves. The Left has trafficked in condescending explanations for the alleged paradox of the right-wing female for quite a long time. The latest in this tired genre, “The Young Women Leaving the New Right” in New York Magazine, is more of the same, dressed up for the digital age.

We are supposed to believe that conservative women are “Pick Mes,” seeking to gain male validation by belittling other women. They are afraid of their right-wing husbands, are too dumb to form their own opinions about politics, have “internalized misogyny,” lack dignity, and so on.

Not even the element of poaching a few disgruntled former conservatives and mining them for embarrassing tidbits is a remotely new tactic. There have always been some willing to take the liberal media up on the chance to open their kimono in exchange for the opportunity to fire a shot at their intra-right nemeses.

Making the Film 'Palestine 36' (w/ director Annemarie Jacir) | The Chris Hedges Report

— —This interview is also available on podcast platforms and Rumble.

In filmmaker Annemarie Jacir’s new film, Palestine 36, one of the most pivotal moments in Palestine’s history is brought to life for the first time through cinema.

In this episode of The Chris Hedges Report, host Chris Hedges speaks with Jacir about the 1936–39 Palestinian uprising against British colonial rule — a mass revolt that laid the groundwork for the modern Palestinian struggle, and also the crushing of Palestine’s organizational infrastructure that culminated into the founding of the Zionist state a decade later.

Film Screening: Tomorrow’s Freedom (17 April)

— Organisation: Free Palestine Melbourne —Progress on gender equality at work is slow and uneven, new index finds

— Publication: Progress in Political Economy —Gender equality at work has barely improved over the past ten years, with paid work opportunities held back by women doing the bulk of unpaid work in the home, new research shows.

Stubborn gaps in pay and career progression, alongside deep division between the types of jobs women and men do, are holding back business and the economy, despite decades of efforts by governments, employers and unions.

To help understand and address these gender gaps, the Australian Centre for Gender Equality and Inclusion at Work has developed a unique tool to measure and track equality at work.

The first Gender Equality @ Work Index provides a comprehensive, national snapshot of gender equality at work over ten years.

Our research shows many of the unequal features of the Australian labour market, such as the concentration of men and women in different industries and occupations, have barely shifted in three decades.

Improvement, but at a glacial pace

Review of Merchant Card Payment Costs and Surcharging – Conclusions Paper

— Organisation: Reserve Bank of Australia (RBA) —February 2026 Media Highlights

— Organisation: The Australia Institute —Our research has been everywhere in February! From Parliament, to TV, to Radio, and social media, watch just a few examples of our impact in February 2026.

The post February 2026 Media Highlights appeared first on The Australia Institute.

03/29/2026 Market Update

— Organisation: Applied MMT —

(Note: Below is a summary of the Market Update Video for 03/29/2026, click here to watch the video update)

Update Preview

Last week finally brought the kind of selling I had been warning about for months. Since the end of 2025, the core argument has been that markets were overpriced relative to flows, and we’re now seeing that mismatch resolve in a much more visible way. The big question now is not whether the selloff was justified — I think it clearly was — but whether this is simply the final shakeout before the next leg higher, or the beginning of something more serious.